The European Union’s economy will experience a deep recession this year due to the coronavirus pandemic, despite the swift and comprehensive policy response at both EU and national levels. Because the lifting of lockdown measures is proceeding at a more gradual pace than assumed in the EU’s Spring Economic Forecast, the impact on economic activity in 2020 will be more significant than anticipated.

As such, the Summer 2020 Economic Forecast projects that the euro area economy will contract by 8.7 per cent in 2020 and grow by 6.1 per cent in 2021. The EU economy is forecast to contract by 8.3 per cent in 2020 and grow by 5.8 per cent in 2021. The contraction in 2020 is, therefore, projected to be significantly greater than the 7.7 per cent projected for the euro area and 7.4 per cent for the EU as a whole in the Spring Forecast.

Growth in 2021 will also be slightly less robust than projected in the spring.

“The economic impact of the lockdown is more severe than we initially expected,” says Valdis Dombrovskis, European Commission vice-president. “We continue to navigate in stormy waters and face many risks, including another major wave of infections. If anything, this forecast is a powerful illustration of why we need a deal on our ambitious recovery package, Next Generation EU, to help the economy. Looking forward to this year and next, we can expect a rebound but we will need to be vigilant about the differing pace of the recovery. We need to continue protecting workers and companies and coordinate our policies closely at EU level to ensure we emerge stronger and united.”

Next Generation EU is not factored into the new forecast since it has yet to be agreed. An agreement on the Commission’s proposal is therefore also considered an upside risk.

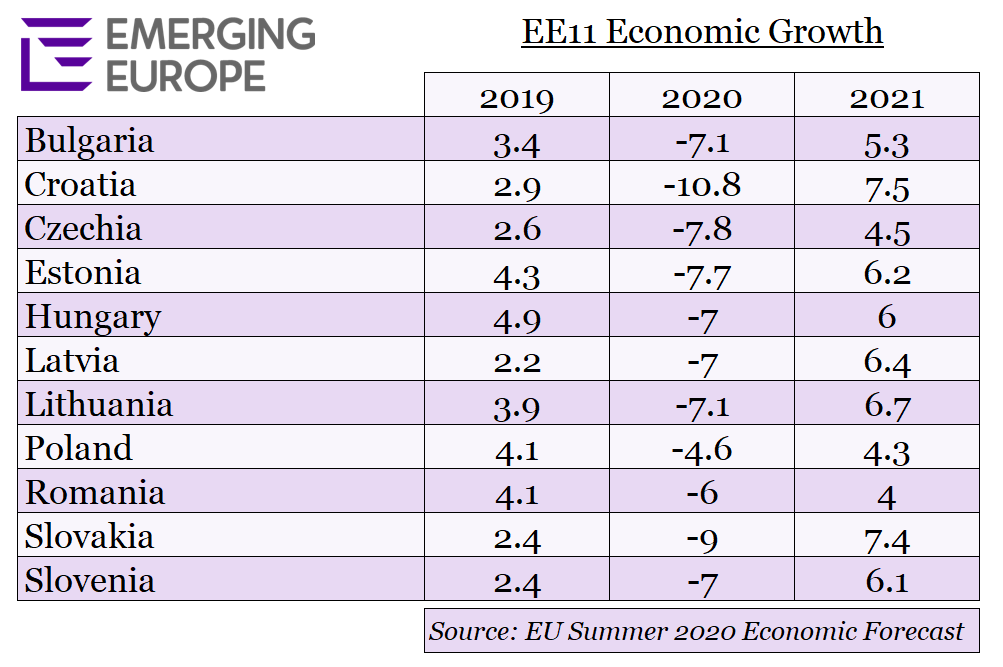

Of the 11 emerging European members of the EU, Croatia is forecast to see the largest contraction, primarily because of the country’s reliance on tourism for almost 20 per cent of GDP.

Poland will see by far the region’s smallest fall in GDP. Poland’s economy proved relatively resilient in the first quarter of 2020, mainly due to its low exposure to hard-hit sectors and diversified economic structure. GDP fell by -0.4 per cent quarter-on-quarter driven by a significant fall in private consumption, while investment decreased only moderately as the construction sector kept expanding and industrial production recorded just a mild contraction.

“Coronavirus has now claimed the lives of more than half a million people worldwide, a number still rising by the day – in some parts of the world at an alarming rate. And this forecast shows the devastating economic effects of that pandemic,” said Paolo Gentiloni, European Commissioner for the economy. “The policy response across Europe has helped to cushion the blow for our citizens, yet this remains a story of increasing divergence, inequality and insecurity. This is why it is so important to reach a swift agreement on the recovery plan proposed by the Commission – to inject both new confidence and new financing into our economies at this critical time.”

The impact of the pandemic on economic activity was already considerable in the first quarter of 2020, even though most member states only began introducing lockdown measures in mid-March. With a far longer period of disruption and lockdown taking place in the second quarter of 2020, economic output is expected to have contracted significantly more than in the first quarter.

However, early data for May and June suggest that the worst may have passed. The recovery is expected to gain traction in the second half of the year, albeit remaining incomplete and uneven across member states.

The shock to the EU economy is symmetric in that the pandemic has hit all member states. However, both the drop in output in 2020 and the strength of the rebound in 2021 are set to differ markedly. The differences in the scale of the impact of the pandemic and the strength of recoveries across member states are now forecast to be still more pronounced than expected in the Spring Forecast.

The risks to the forecast are exceptionally high and mainly to the downside.

The scale and duration of the pandemic, and of possibly necessary future lockdown measures, remain essentially unknown. The forecast assumes that lockdown measures will continue to ease and there will not be a ‘second wave’ of infections. There are considerable risks that the labour market could suffer more long-term scars than expected and that liquidity difficulties could turn into solvency problems for many companies. There are risks to the stability of financial markets and a danger that member states may fail to sufficiently coordinate national policy responses. A failure to secure an agreement on the future trading relationship between the UK and the EU could also result in lower growth, particularly for the UK. More broadly, protectionist policies and an excessive turning away from global production chains could also negatively affect trade and the global economy.

There are also upside risks, such as an early availability of a vaccine against the coronavirus. More generally, a swifter-than-expected rebound cannot be excluded, particularly if the epidemiological situation allows a faster lifting of remaining restrictions than assumed.

The European Commission’s next economic forecast will be the Autumn 2020 Economic Forecast which is scheduled to be published in November 2020.

—

Unlike many news and information platforms, Emerging Europe is free to read, and always will be. There is no paywall here. We are independent, not affiliated with nor representing any political party or business organisation. We want the very best for emerging Europe, nothing more, nothing less. Your support will help us continue to spread the word about this amazing region.

You can contribute here. Thank you.

Add Comment